.svg)

Solving the dry year

New Zealand is well-endowed with natural resources that we have harnessed to run our homes, farms and businesses. We are very reliant on hydro storage for electricity but when it doesn't rain, we need to rely on other sources. So what's the best way to plug that 'dry year' gap as we wait for more renewable resources to come online?

New Zealand’s energy system is mostly run on imported fuels. Around 25% of our energy comes from electricity and around 60% of that electricity comes from hydro. We are very reliant on the big wet battery known as our storage lakes to get us through winter when demand for electricity is highest and when there is no rain, we need to rely on other sources.

We experienced dry years in 2001, 2003, 2008, 2012, 2017, 2019, 2021 and 2024 and when the lakes get low, we typically ‘firm’ or back up our hydro reserves with fossil fuels, mostly gas, coal and sometimes diesel. These fuels are the most expensive form of generation and set the price for the whole market.

The wholesale price generally fluctuates between $90 and $150 per MWh but often shoots up during dry years and in 2024, it reached a massive $800.

So how do we solve it?

Jump to sections

- The current situation

- For and against?

- A better back up

- Could renewables do it?

- The international context

- Will the price of LNG come down

- What else do we need?

- Regional revival

- The wash -up

TLDR? Check out our infographic

The current situation

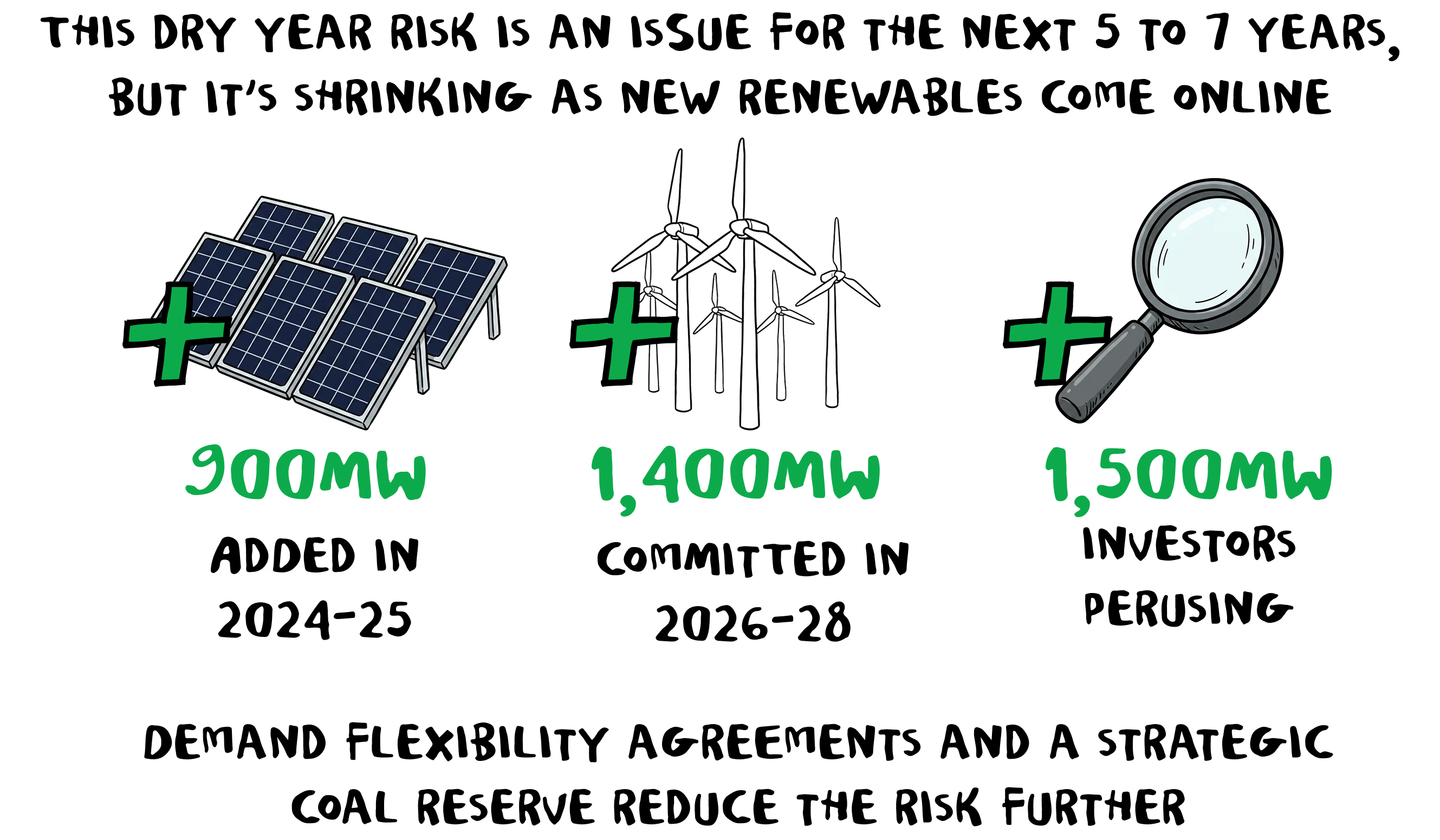

There is a potential shortfall of around 1.5 TWh in a dry year (for context, the country uses about 40 TWh every year). But that number is shrinking as more renewables like wind, solar and geothermal come online.

Over 900MW of new distributed and grid scale renewable generation was added in 2024 and 2025. There is 1,400MW of grid scale generation committed to come online from 2026 to 2028 and a further 1,500MW being actively pursued by investors (in layman’s terms, MW is how big a power source is and TWH is the amount of energy that can be generated or consumed over time).

That leaves a few years where we might have a shortfall and, with domestic gas reserves running low, this is the primary reason the LNG terminal has been proposed.

Recent news showed that domestic gas reserves had fallen to a 20-year low as major fields declined faster than expected and reserves declined 23 percent from last year.

There is also a suggestion that LNG could be used to support large industrial gas users, but the issue is that LNG is much more expensive than domestic gas and this would just lock them in to an unproductive business (and potentially require future Governments to subsidise them).

Electricity demand is growing and we need affordable, secure energy to increase our prosperity. Associate Energy Minister Shane Jones has said there is no economic plan without an energy plan and that net zero is a nice idea but it can’t come at the expense of hollowing out our economy. We agree. But we also don’t want to waste “north of a billion dollars” on a Liquified Natural Gas import terminal that may never get used and will only increase electricity prices if it does, especially as there is another back-up option that is cheaper, faster and more beneficial to the wider economy.

For and against?

MBIE’s modelling has shown that we only need an LNG terminal in extreme circumstances.

Some big gas users have said we need it, as evidenced by an ad in the NZ Herald from Galvanising NZ, NIG Nutritionals and some bakeries. And the Government’s standard line is that we cannot rely on the weather and we need firming options to keep the lights on and prices low “when the sun's not shining, the wind's not blowing, and the lakes are low”.

But there are not many in favour of the LNG terminal - or the fact that it will be funded through a levy on all electricity users - especially as prices surged after the Middle East conflict kicked off.

There is a lot of discussion within the energy sector suggesting we don't need a long term LNG dry year solution, and we agree.

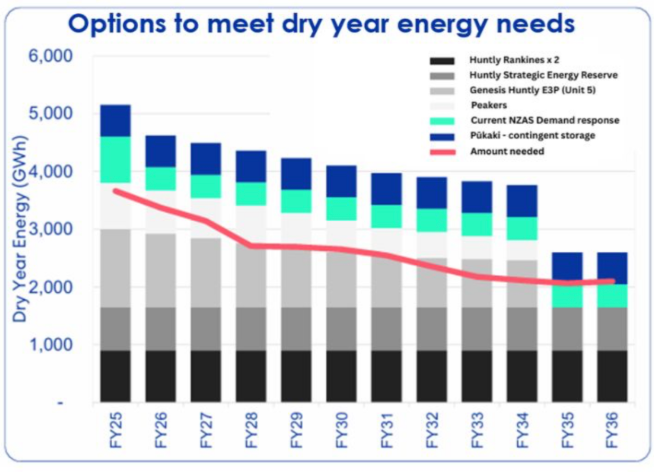

Meridian has said LNG is not needed for dry year cover. It stated that “New Zealand’s dry year risk is reducing” and that “the more renewables that are built, the more we can protect the storage in our hydro lakes and the Huntly stockpile [agreed to by all the gentailers and approved by the Commerce Commission], and the better that is for New Zealand.”

Coal is more about providing baseload power but it is still an option that can work alongside diesel as a back up (more on that below).

Speaking at a Select Committee hearing, Meridian CEO Mike Roan also pointed out that solar is well-suited to dry years as higher production can help keep the lakes full.

Our research has shown that solar can provide an extra 11% in the critical months during a dry year versus non-dry years and, importantly, this generation can be added much more quickly than other large renewable projects.

Meridian’s graph shows New Zealand’s dry year risk is reducing every year and does not require a high capex, long-term solution.

Meridian has also argued for more access to water storage. This is still to be debated, but the way hydro is used could definitely be improved and it needs to be seen as the county's most valuable battery, where we ‘pre-emptively’ firm with renewables.

Contact’s Mike Fuge also said the dry year risk is declining and at the Murihiku Regen conference he said the deindustrialisation of New Zealand due to a shortage of gas was a myth because there is so much more renewable generation locked in and many processes that can now be electrified.

Agreements with big electricity users like Tiwai and NZ Steel that allow electricity to be redirected during dry years also reduces the risk.

Genesis CEO Malcolm Johns said that the LNG terminal was short for “Likely No Gas” at an event after the Middle East conflict started and a $200 million capital raise that the Government supported will be used to build more wind and solar farms and grid-scale batteries, and extend the life of the Huntly Rankines, with the potential to use biomass if they can make the economics work. Genesis has also talked about using hydro better alongside solar.

In May, Mercury said it supports market-led responses to security of supply risks.

“The market is already responding through new renewable generation, geothermal development, hydro refurbishment, batteries, demand response, long-term customer contracting, gas flexibility arrangements, and the Strategic Energy Reserve (SER) / Huntly Firming Option (HFO) arrangements … Mercury broadly considers the Draft SOSA's conclusion that winter energy risk may emerge in the early 2030s to be reasonable. However, there remains time for the market to respond - as it already is.”

We agree that the dry year risk is getting much much smaller and an expensive solution like an LNG import terminal is not warranted, but there are still those who see remaining risk and for them we have a much better back up option.

A better back up

A new report, produced by independent energy experts Sapere, shows that an LNG terminal is a short-term reaction with long-term consequences. It says the Government did not fully consider whether a new dedicated dry-year fuel is even necessary, and did not do a robust comparison with the other options.

- Download the report here.

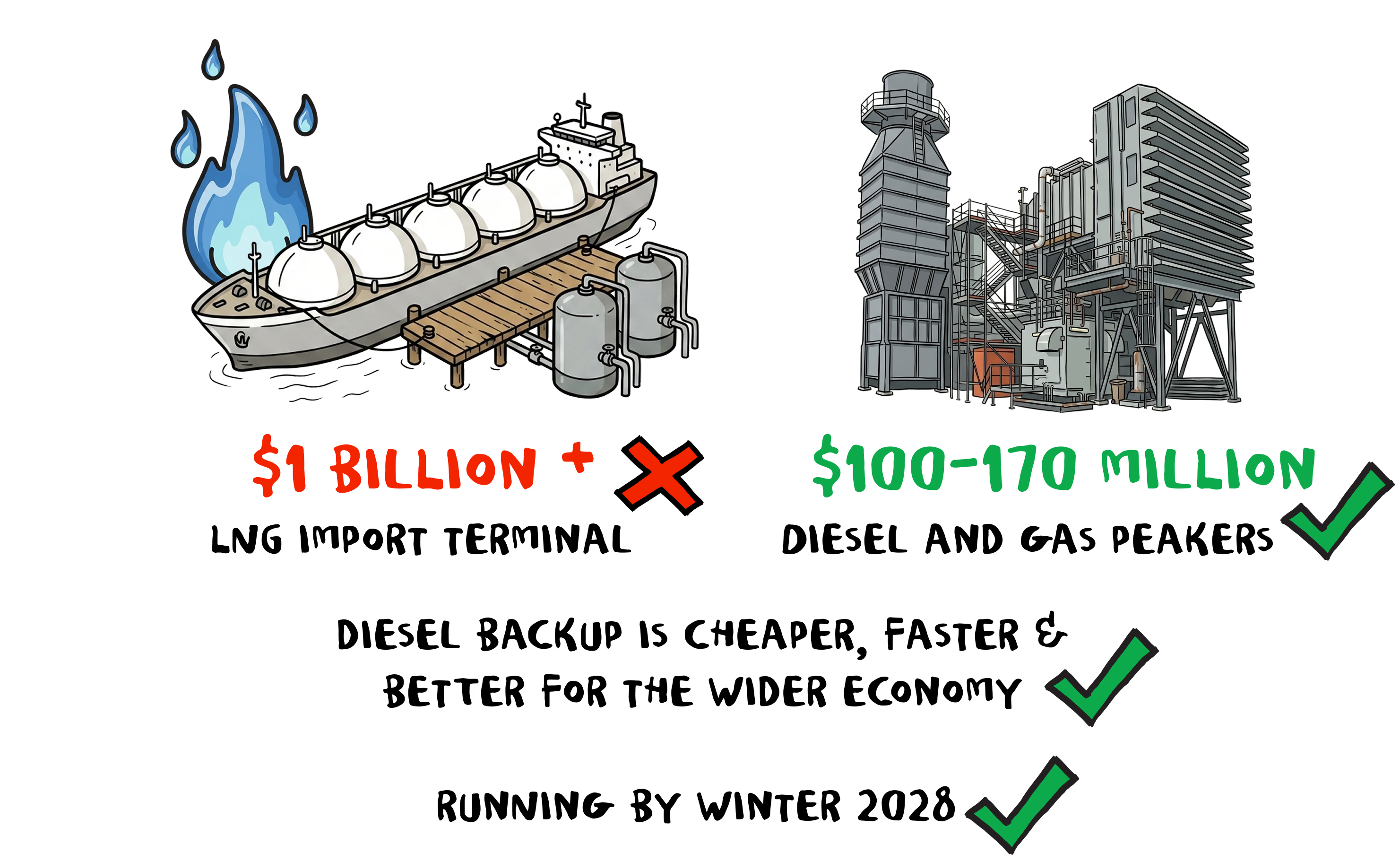

The report shows that diesel can solve the near term risk of a dry year gap for the next 5 - 7 years and it is favourable in terms of cost, timing, and broader economic resilience and the advice MBIE gave the Government that ruled out diesel as a dry year solution was flawed in a number of ways.

The conversion of 400MW of existing gas peakers to run on either gas or diesel, with sufficient back up diesel storage, is a straight forward solution that:

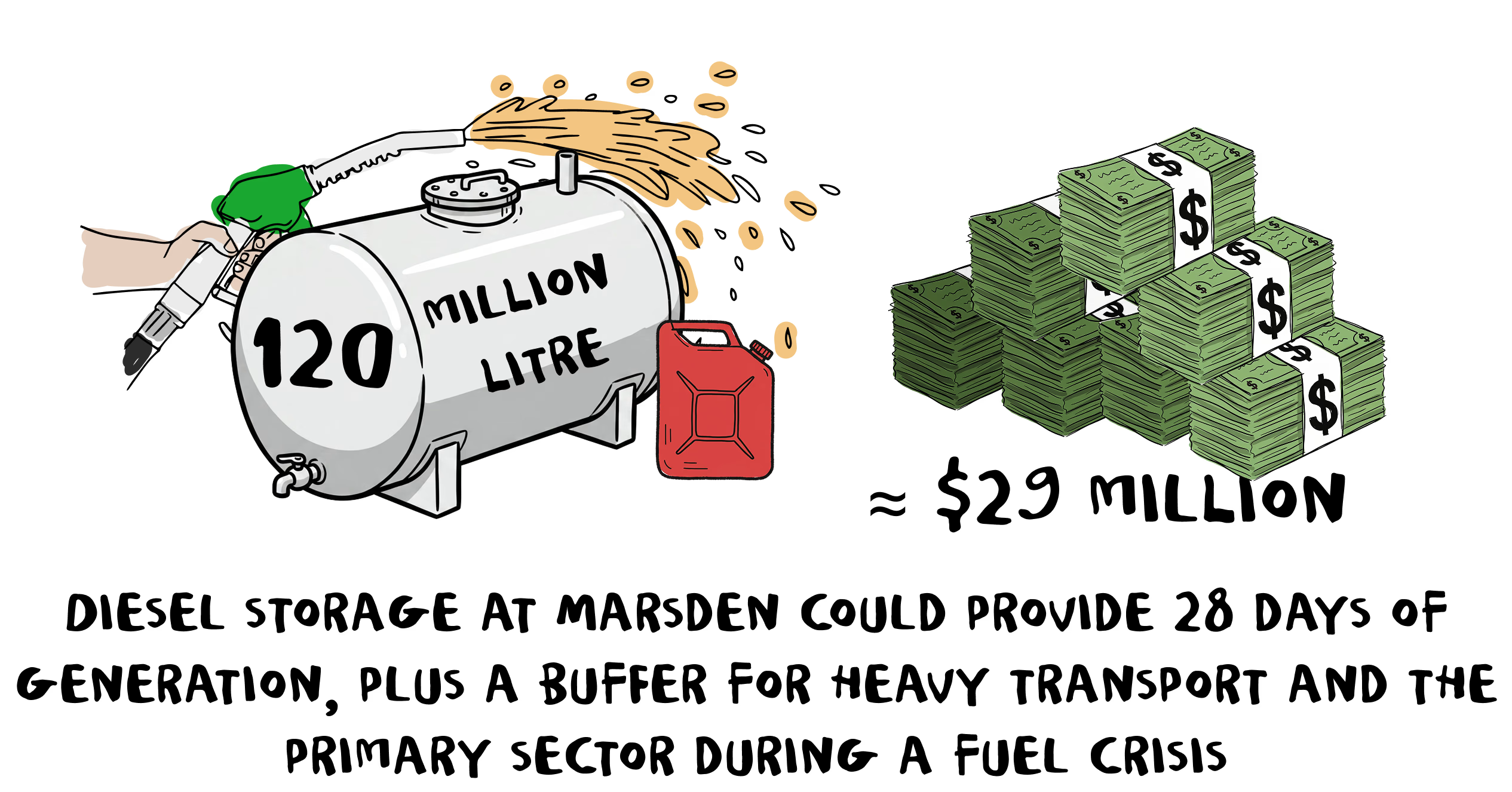

- Could cost as little as $154 million, compared to “north of a $1 billion” for LNG.

- Be delivered before winter 2028, utilising off the shelf kits that take about 15 days to install

- Includes 120 million litres of additional diesel storage, providing 28 days of generation. This would provide a buffer to allow time for additional diesel deliveries in the unlikely event of a bad dry year.

- The additional diesel storage would greatly improve the resilience of our primary sector and trucking fleet, if there is another fuel crisis.

Based on the price the Government has paid to recommission 90 million litres of storage at Marsden Point, recommissioning a further 120 million litres of storage for diesel would cost less than $29 million. A coastal shipping solution would also be required to deliver this to Whirinaki (Port Napier), and Todd and Contact’s gas peakers (Port Taranaki).

Diesel will be required for many more years as we transition to electric machines running on New Zealand-made Energy, so it makes sense to invest in extending existing diesel infrastructure rather than creating a new dependency.

Diesel is a cheaper upfront solution, but would be more expensive to operate. Changes to contracts would insulate businesses from high costs in a dry year, however.

Could we do it with renewables?

If we wanted to create a different back up system with renewables, it is technically possible but, like any portfolio, diversification is a good strategy.

For example, we could build an 800MW wind farm and only turn it on for the dry year (it would need to be kept separate from the wider electricity market and investors would need to be incentivised to build it).

As our previous explainer detailed, if a 9kW system was installed on 50% of homes in New Zealand, the 11% bump in that period would equate to 225GWh of ‘extra’ production in a dry year.

If 30,000 farms had a 300kW system (around 600 panels) that would equate to the same amount of extra production in a dry year.

That’s around 5% of New Zealand’s total hydro storage capacity.

If it had been there in 2024, it would have equated to an extra 18 days of hydro storage, based on the trajectory of national storage in July/August.

5% or 18 days might not sound like much, but when hydro storage bottomed out in 2024, the average wholesale price averaged 80c/kWh for a week, with coal and gas generation setting the price. 18 days earlier, when hydro storage was higher, the wholesale price averaged only 37c/kWh for that week.

If we had that extra solar capacity, all other things held equal, the worst prices we would have seen would have been 37c/kWh. So it is fair to say it would have more than halved the wholesale price at the worst time of the crisis because solar would have kept more water in our lakes.

The international context

The Prime Minister has recently started saying that we need energy independence for national security. But energy independence doesn’t come on ships or from signing up to a new fossil fuel subscription.

Lower energy costs mean higher productivity. And while the Government has estimated it will save $50 per year by removing the ‘dry year premium’, many believe LNG will actually drive up costs for customers, including respected economists from the OECD.

Our electricity market is currently not exposed to international gas prices, and the OECD said it was not wise to start now.

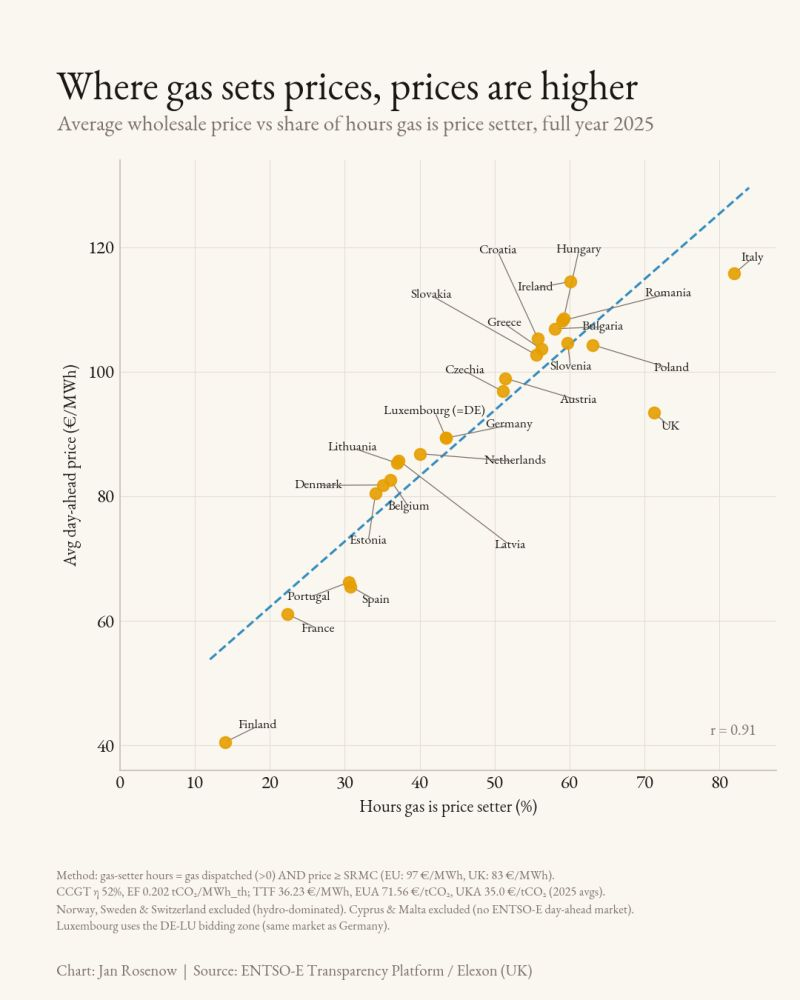

Countries with more electric transport have been able to better insulate themselves from high fuel prices and countries where the electricity price was more closely tied to renewables - like Sweden, Finland, Norway, Canada and Iceland - have been able to keep electricity prices low.

Countries that have their electricity price tied to gas are more exposed to higher prices, as this graph of European wholesale prices shows.

Many Asian countries like Taiwan, Singapore and Japan are very reliant on LNG and Japan is now mulling a US$3 billion subsidy scheme to help users through the current price spike from July.

High energy prices in New Zealand have been blamed for multiple business closures in recent years, but cheap electricity should be seen as a solution to the deindustrialisation and productivity issues we are currently witnessing. Bringing in LNG to give certainty to gas users is basically a long-term subsidy that locks those businesses into volatile, high-cost fuel, so it will exacerbate the problem.

Will the price of LNG come down?

LNG prices effectively doubled overnight after the conflict started and the Strait of Hormuz was closed. Around 20% of global supplies go through the strait and some LNG infrastructure was badly damaged. Qatar, one of the world’s biggest producers, says sites will take years to fix.

While prices have come down since, the International Energy Agency, The World Bank and International Monetary Fund have all said the price of all fuels will remain high for an extended period.

The head of the International Energy Agency, Fatih Birol said the oil crisis has changed the fossil fuel industry forever and countries are now turning away from fossil fuels to secure energy supplies because their perception of risk and reliability has changed.

"The vase is broken, the damage is done – it will be very difficult to put the pieces back together. This will have permanent consequences for the global energy markets for years to come.”

The World Bank estimates energy prices will increase by 24% this year and the International Monetary Fund has suggested fuel prices will remain high for a prolonged period due to supply disruptions and infrastructure damage.

Just after the conflict started, Infometrics’ Brad Olsen said: “Very quickly, the risks outlined around LNG access have come true. Current events make it harder to immediately buy into why this LNG facility is likely the best option, because it has potentially fallen over at the first hurdle."

Even Exxon Mobil CEO Darren Woods said: “If you look at the unprecedented disruption in the world’s supply of oil and natural gas, the market hasn’t seen the full impact of that yet.”

His colleague Neil Chapman said: “We’re approaching unheard of inventory levels. I mean really, really low levels. You can debate whether that’s going to hit those really low levels in two weeks or three weeks. Once you get to that point, then you’ll see prices shoot up.”

As countries eat into their strategic reserves and the Strait remains closed, low oil and gas stocks will need to be replenished and that won’t happen overnight.

Even if prices do eventually come down, relying on LNG means our economy will be even more exposed to the vagaries of geopolitics and it’s a question of when, not if, the next global disruption will occur.

What else do we need?

It’s not just as easy as upgrading the peakers and increasing diesel storage, however. Significant changes will also be required to the electricity contracts market, to ensure the lowest cost solution to dry year (i.e. renewables) will actually be built and secure supply can be bought. That is every bit as important as the infrastructure as it needs to deliver affordable insurance to our large electricity-hungry businesses, protecting them against volatile wholesale prices in a dry year.

Sapere’s work looks across the wider energy system, including looking at the future of the gas industry and the role of LNG as a replacement.

It evaluates options on how to best improve overall energy system security and resilience, including for existing industrial and large commercial gas users.

LNG prices are expected to stay high and will only delay the transition to a more stable, more secure, more productive future and the money would be better spent on helping to electrify these businesses.

Given the shortage of domestic gas, more work needs to be done to help industrial users transition to electricity for process heat - over and above the Government-backed loan scheme announced recently, which the Sapere report said was a "tepid" response. This policy was an admission that gas has no future in New Zealand and that access to finance was a crucial part of the transition.

Supporting industrial users to get off gas will require some investment into our regions, but this would also cost less than the ‘$1 billion plus’ bill for LNG, and stretch our remaining domestic gas reserves out for around an extra two decades and allow it to be used by businesses with no options to switch. It will also be much more likely to keep existing jobs and create new ones in those regions.

Our analysis shows that around one third of gas users could transition now with loans, one third would require a subsidy and one third have no option - yet.

Just as those hoping to electrify their homes are put off by the upfront costs, so are businesses. It remains the biggest barrier, but many businesses are electrifying anyway and taking things into their own hands.

The European Bakery in Queenstown, while relatively small by commercial standards, is upgrading its gas ovens to electric over time and has worked with its landlord to install solar and batteries to ensure it gets access to the cheapest electricity to run them.

NZ Steel is set to commission its $300 million electric arc furnace soon and Hayes Metals in Auckland has been running an electric smelter for a few years, while EECA has facilitated grants to a number of businesses upgrading to electricity, from Speight’s Brewery’s 3MW electrode boiler in Dunedin to Van Lier Nurseries 1MW heat pump for its greenhouses.

High temperature heat pumps, while relatively new technology, are advancing quickly. As Oxford energy professor Jan Rosenow explained: “A huge share of industrial energy demand sits below 200°C: food and drink, paper, textiles, parts of chemical industry etc. That range is now squarely within reach of commercial heat pumps you can order today. The technology isn't the bottleneck anymore. The bottleneck is policy, grid access and electricity prices. Where power is cheap relative to gas, the business case is already there. Where it isn't, it's primarily a tax and tariff problem, not an engineering one.”

Network upgrades may be required for these big users to transition and it is good to see that EECA has been given $6 million in additional funding in the latest budget to assist them. More could be done to guide businesses through this often complex process and potentially negotiate with EDBs to keep the costs in check.

While demand for electricity has been relatively stable for many years, demand is increasing now as industrial processes, transport and gas hot water and heating are electrified. Estimates suggest we will need to double the amount of electricity generation by 2050. We need more big stuff like wind, solar and geothermal and, with the right incentives in place and demand for electricity growing, that will be built. But we also need more small stuff.

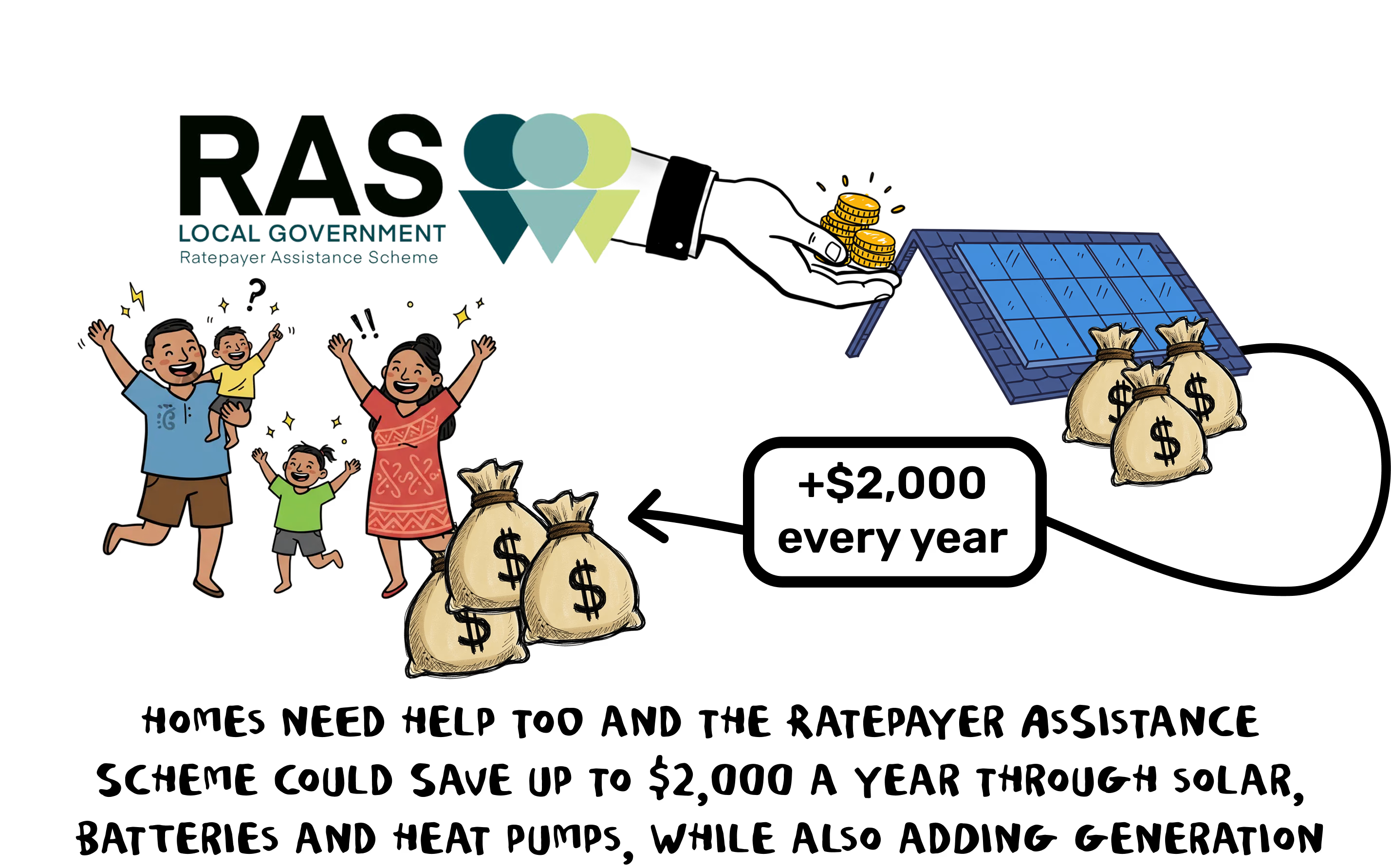

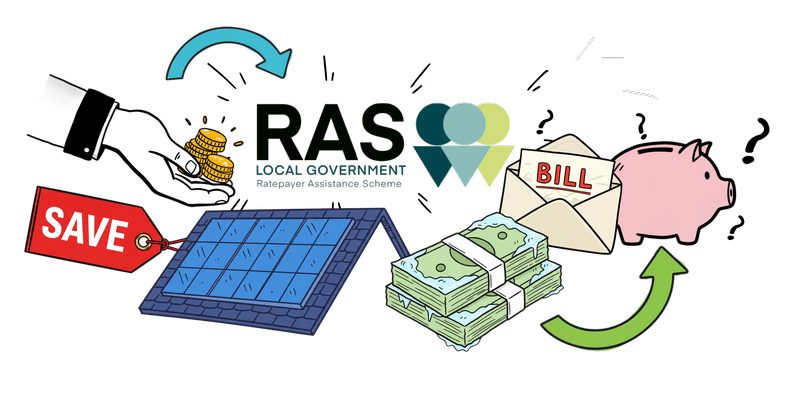

Unlocking affordable long-term finance for solar, batteries and electric heating for households and SMEs through the Ratepayer Assistance Scheme is crucial. This would remove upfront cost barriers and could save a typical gas-dependent household around $2,000 per year including repayments. It will also rapidly increase the renewable generation we need. As we have seen in many other markets, solar is displacing fossil fuels for electricity generation overall, while batteries large and small are displacing gas for daily peaks.

The RAS would be especially beneficial to older constituents who may own their own home, but are struggling to pay their bills.

Reviving the regions

Renewables are, by their nature, regional. Large projects - from industrial transitions to big wind and solar farms to network upgrades - will keep the money flowing in the provinces (in Australia, large renewable projects were listed as the only thing keeping New South Wales out of recession recently).

The LNG terminal would provide Taranaki with a short-term boost, but that is just one region and over 100 people turned out in New Plymouth recently to protest against it - due to costs, emissions and safety. Solar, on the other hand, will create jobs right across the country.

The energy transition desperately needs more sparkies and plumbers and an extra $69m over four years to double the number of students at Trade Academies to 20,000 by 2030 will help.

There are around 10 million fossil fuel machines in New Zealand and about 8.5 million of them are ready to be electrified right now. Every one of them will need to be charged and maintained and many of them will require upgrades to existing infrastructure in homes, farms and businesses. There will be hundreds of thousands of solar panels, batteries, EV chargers, cooktops and hot water heat pumps to install.

While there is obvious concern about the decline of the gas industry, going electric could be one of the biggest job creation moments in New Zealand history and offer jobs across the regions in important industries by securing their energy for the decades to come.

The wash up

New Zealand is well-endowed with natural resources that we have harnessed to run our homes, farms and businesses. More renewable resources are coming and cheap, abundant energy running through electric machines is key to the country's prosperity, but there may be a gap to plug. In the short-term, the dry year risk is real. But it is a national risk that we are attempting to solve by importing a larger international risk.

Sapere’s rigorous analysis shows the LNG import terminal is not the best option and the money would be better spent on a diesel back-up option and more help for gas users to transition to electricity.

We already import diesel and having more of it in storage has wider economic benefits. And if we build the renewables fast enough, ideally we won’t even need to use it.

The industry is developing market-led solutions like demand agreements and strategic coal reserves and solar is a particularly good partner for hydro as it produces more in a dry year.

If the question is dry year, LNG is not the best answer in the short or long-term. If the question is a shortage of gas for businesses, LNG is not the best answer.

.jpg)

Related posts

More Watt Now? posts from Rewiring Aotearoa

Solving the dry year

Read More

.png)

Sun in a socket: plug-in solar

Read More

The case for energy loans

Read More

A bad case of gas

Read More

Scale and speed: why the climate needs electric vehicles

Read More

A future with two visions

Read More

Show me the money: the economics of going electric

Read More

Why electric vehicles matter

Read More

Why solar makes sense

Read More

Why going electric wins on emissions

Read More

Energy use in New Zealand

Read More

Closing The Loop

Read More

Electricity means efficiency

Read More